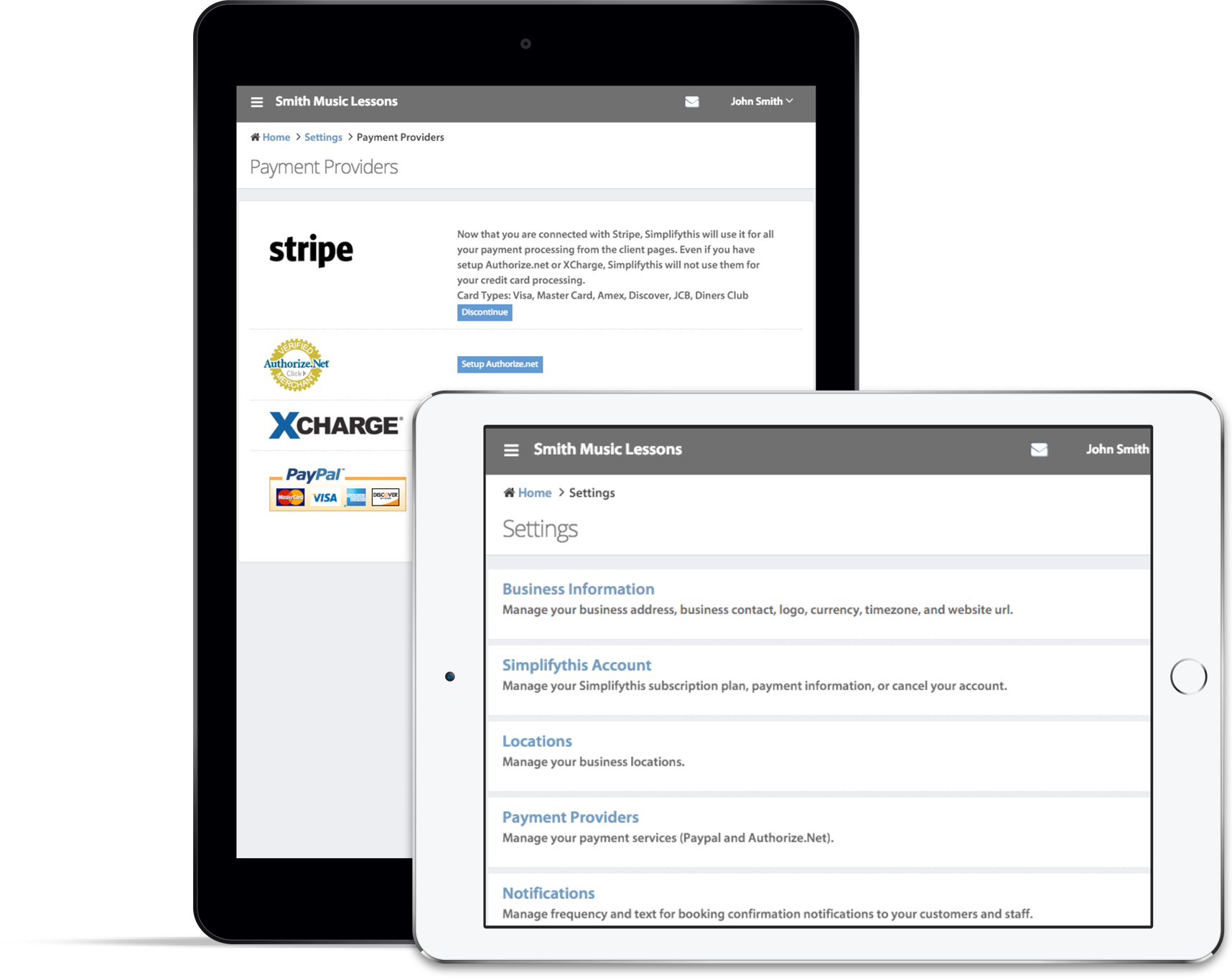

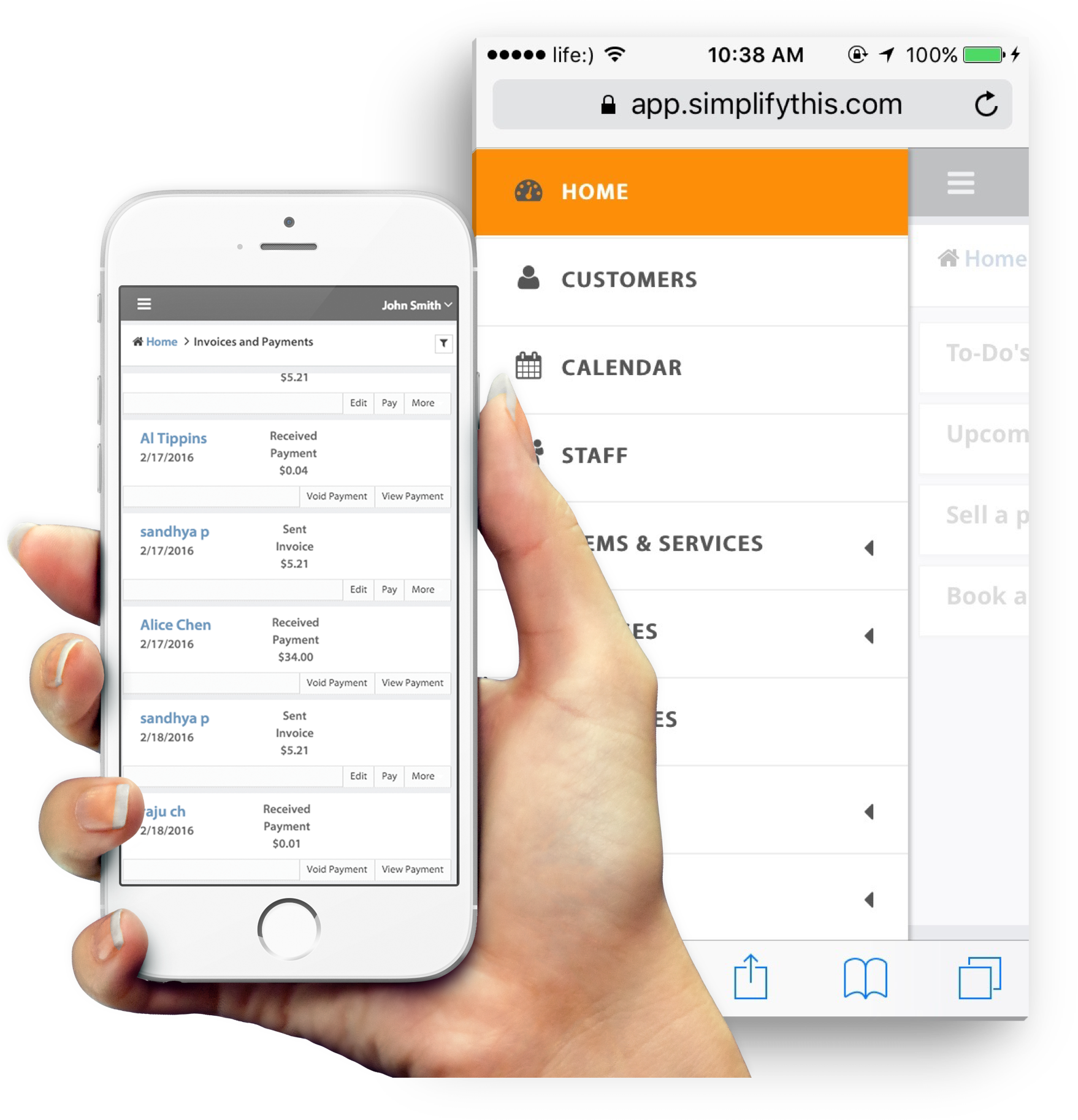

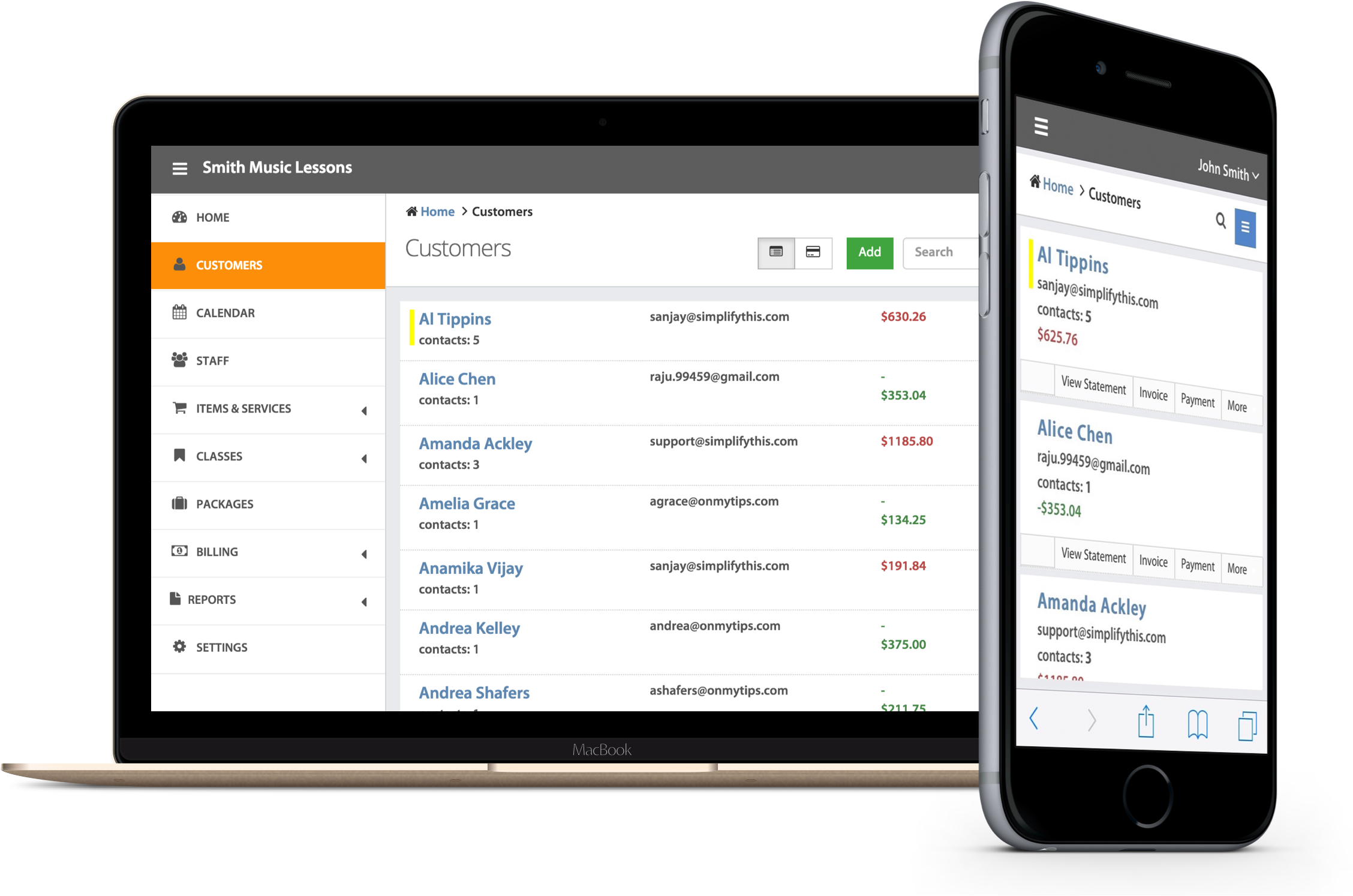

Use any Device

SimplifyThis works with your computer, iPhone, Android or tablet, just use your favorite browser and SimplifyThis automatically adapts to your device. Android users can also download the Android app from the Google Play store.

You can access SimplifyThis from your computer, Android phones and tablets, iPhones and iPad, and Windows phone. Download the SimplifyThis app for Android devices from Google Play store. iOS apps are coming soon! In the meantime, you can use your browser from iPhone or iPad to access SimplifyThis.